CFDs vs. Micros Eminis

Micro Eminis trade on centralized markets, so why trade CFDs when you can trade Micro Emini Futures?

Lots of traders buy and sell commodity Contracts for Difference, more popularly known as CFDs. And they typically believe that they are trading a “futures” equivalent. And why not? If the underlying futures go up on price, they make money. If the underlying falls, they experience loss. But the difference, large or small, is real. And so too are the consequences. Let’s dispel the hype and get to the reality of the situation.

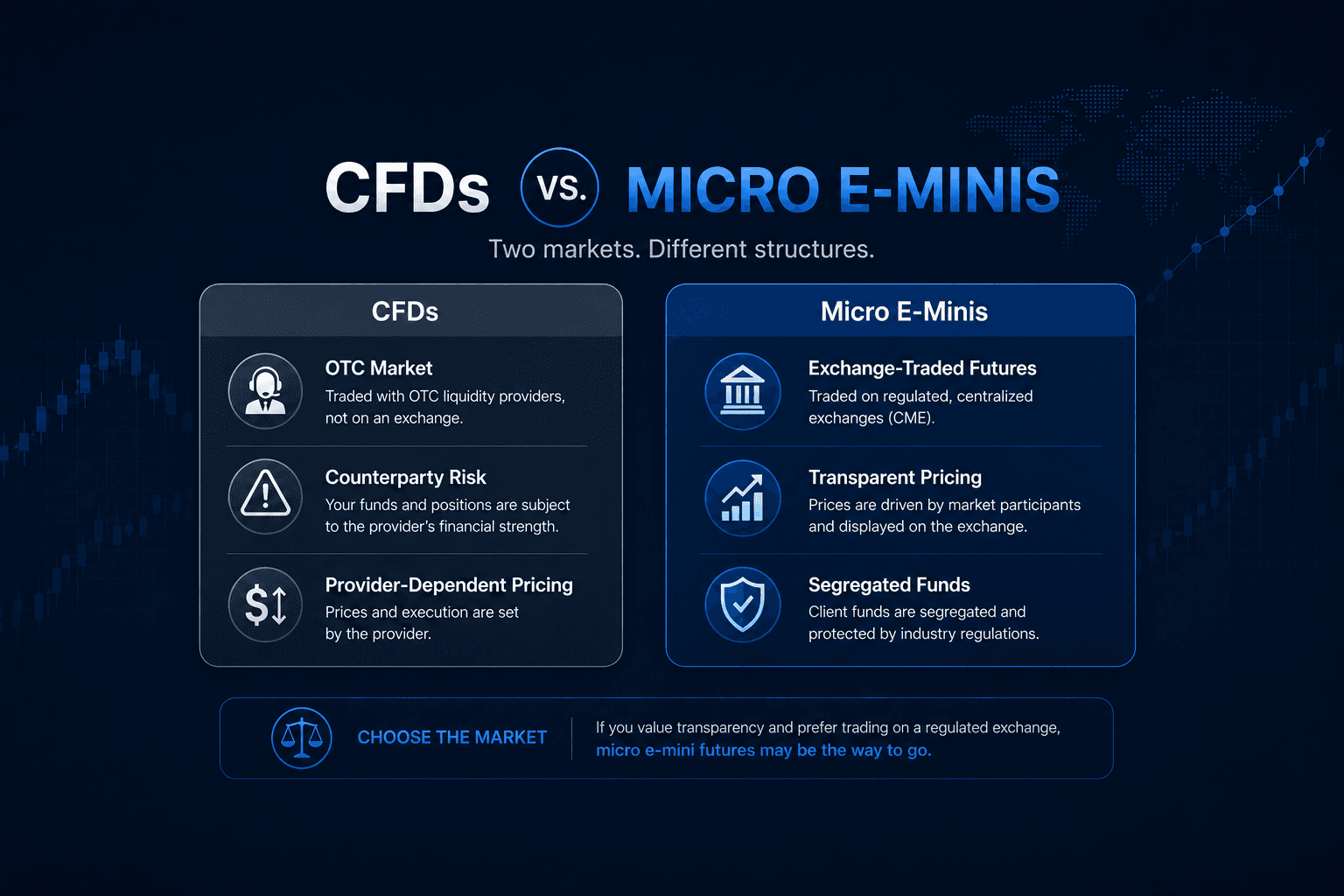

Unlike centralized futures exchanges, CFDs are typically traded through over-the-counter liquidity providers. Here’s how that structure works.

Let’s suppose that you want to trade the e-mini S&P 500 futures (ES). For some reason, you are unable to trade the actual ES futures contract, so you decide instead to open an account with an over-the-counter “liquidity provider” (LP) who promises to give you the same futures “exposure” as the actual contract but with greater flexibility in lot size and lower margins.

You open an account, and for your first trade, you buy the smallest S&P 500 contract available: it moves $1.25 for each tick, or $5.00 per point. As a buyer, your order gets filled by the LP who just sold your lot. In other words, the LP is on the other side of your trade.

The outcome of your trade is one of the following:

- If you lose money on your trade, the LP simply takes the money out of your trading account.

- If you made money on your trade, the LP is obligated to credit to your account.

Keep in mind that you didn’t actually possess the actual futures contract (the ES), and the LP might or might not have possessed it either. There’s a possibility that nobody actually possessed a futures contract. You, the trader, simply bought a “promissory contract” that the LP will either debit or credit your account.

HERE’S WHAT CAN GO WRONG:

CFD Trading Gone Bad – Example 1:

If the LP controls the entire transaction, from price quote to order fill, they can technically raise or lower the bid and ask price to make a profit:

- You place a buy stop for the S&P 500 at, say 2840.00

- Suppose they raise the ask to 2840.25 so when your buy stop becomes a market order, you bought it at their price.

- Meanwhile, let’s suppose they were able to buy the ES at 2840.00.

- The LP just bought “low” (2840.00) and sold it to you “high” at 2840.25–they arbitraged you for 0.25 points.

Now, what difference does 0.25 points make? An LP can do this all day long using automated software, and if they do it enough times, they can generate a decent profit.

In contrast to the futures market where price is transparent and driven by market participants, you run the risk of not getting filled at a fair price when trading with an LP.

CFD Trading Gone Bad – Example 2:

Let’s imagine that the broader U.S. stock market is soaring. You bought a huge CFD position on the S&P 500. But so did thousands of other clients trading with your LP.

Suppose the LP who sold the CFDs to these clients did not fully hedge its exposure. In that case, the LP may be on the opposite side of a significant amount of client trading activity, effectively carrying “short” exposure against those CFD positions.

If clients are generating substantial gains, the LP could face corresponding losses. And if the LP is not adequately hedged (for example, by purchasing ES futures contracts or other offsetting instruments), it may be responsible for covering those client gains. Depending on the LP’s risk management practices and financial resources, significant market moves could place financial strain on the provider and increase counterparty risk to clients.

In some cases, LPs aren’t required to keep client funds segregated. This means that client funds may be used as part of the LP’s operating capital. So if they go bankrupt, their customers may lose anywhere from a portion to the entirety of their funds.

Lets take a look at the alternative: Regulated Exchanges for Futures Trading

Futures, on the other hand, are traded on a regulated exchange. Prices are transparent and market driven. Client funds are required to be segregated. And exchanges are required to hold reserve funds to help reduce credit risk. Please do remember that there are still risks involved with futures trading, and that even properly segregated client funds may be at risk in the event of an FCM’s bankruptcy. That said, it is our opinion that the regulations related to counterparty transparency and customer fund segregation in the futures trading industry are stricter than with CFD industry.

If you trade CFDs only because they offer smaller lots than the standard emini futures, then you might want to consider the new micro e-mini equity index contracts, which have recently been launched.

The micro e-mini futures are a smaller version of the standard emini index derivatives for the following U.S. stock indices: S&P 500, Dow Jones Industrial Average, Nasdaq 100, and Russell 2000.

Their symbols:

- Micro Emini S&P 500 – listed as MES

- Micro Emini Dow Jones – listed as MYM

- Micro Emini Nasdaq 100 – listed as MNQ

- Micro Emini Russell 2000 – M2K

How do they “tick” in terms of minimum dollar value?

The value of each MES contract is $5 times the S&P 500 index; MYM, $0.50 times the DJIA index; MNQ, $2 times the Nasdaq 100; and M2K, $5 times the Russell 2000. This means that the MES moves $1.25 per tick (per contract);and the MYM, MNQ, and M2K all move $0.50 per tick (per contract).

These dollar-per-tick values are as low, if not lower, than most CFD values.

But here are the differences:

- Micro futures are traded on an exchange (not dealt to over the counter).

- Because micro futures trade on regulated exchanges, pricing is driven by market participants rather than a single liquidity provider.

- Micro futures are highly-regulated instruments.

If you value transparency and prefer to trade in a “real” market on a regulated exchange, then micro emini futures may be the way to go. To learn more about these instruments, contact us at GFF Brokers.

Please be aware that the content of this blog is based upon the opinions and research of GFF Brokers and its staff and should not be treated as trade recommendations. There is a substantial risk of loss in trading futures, options and forex. Past performance is not necessarily indicative of future results.