Upcoming Government Reports & Holidays

| 1-Jan | NEW YEAR’S DAY |

|

3-Jan

|

CONSTRUCTION SPENDING REPORT |

|

8-Jan

|

INTERNATIONAL TRADE REPORT |

|

7-Jan

|

MANUFACTURERS’ SHIPMENTS, INVENTORIES & ORDERS REPORT |

|

8-Jan

|

US INTERNATIONAL TRADE IN GOODS & SERVICES REPORT |

|

4-Jan

|

EMPLOYMENT SITUATION REPORT |

|

10-Jan

|

MONTHLY WHOLESALE TRADE: SALES & INVENTORIES REPORT

|

|

10-Jan

|

WHOLESALE TRADE REPORT

|

|

15-Jan

|

PRODUCER PRICE INDEX REPORT

|

|

11-Jan

|

CONSUMER PRICE INDEX REPORT

|

|

16-Jan

|

ADVANCE MONTHLY SALES FOR RETAIL & FOOD SERVICES REPORT

|

|

16-Jan

|

MANUFACTURING AND TRADE: INVENTORIES & SALES REPORT

|

|

17-Jan

|

NEW RESIDENTIAL CONSTRUCTION REPORT

|

|

25-Jan

|

ADVANCE REPORT ON DURABLE GOODS

|

|

30-Jan

|

GROSS DOMESTIC PRODUCT REPORT

|

|

21-Jan

|

MARTIN LUTHER KING, JR DAY

|

|

25-Jan

|

NEW RESIDENTIAL SALES REPORT

|

|

29-Jan

|

ADVANCE ECONOMIC INDICATORS REPORT

|

Key Events That Moved the Market in December 2018

The following is a review of US and world events from the last month. Please be advised that this content is based upon the opinions and research of GFF Brokers and its staff and should not be treated as trade recommendations.

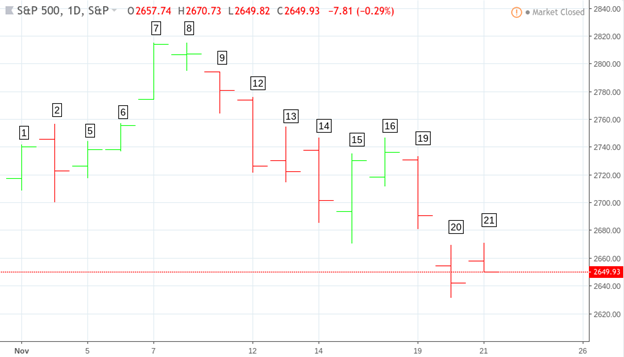

Above: S&P 500 Index Daily Chart from December 3 – 21, 2018

December 3

- Stock indices surged on news that Washington and Beijing agreed to a 90 day trade ceasefire.

- President Trump reported that China has agreed to remove tariffs charged on vehicles made in the US to below the 40% level.

- The White House also said that the existing tariffs on 10% of Chinese products (currently worth $200 billion) would be increased to 25% if no agreement was reached within 90 days.

December 4

- Stock indices plunged when conflicting reports regarding the US-China agreements were made public.

December 5

- Markets were closed in honor of President George H.W. Bush’s passing.

December 6

- Stocks declined as the arrest of a top executive of Chinese tech giant Huawei for extradition to the U.S. from Canada triggered doubts over the prospects of US-China deal within in the 90-day truce period.

- Stock index futures recovered most of its losses due to a report that the Federal Open Market Committee will scale back its interest rate hike schedule next year.

- Weekly U.S. jobless claims declined 4,000 to 231,000, not quite meeting consensus expectations called for initial claims to be 226,000.

- U.S. worker productivity increased at a faster rate in the third quarter than initially estimated. Productivity of non-farm workers rose 2.3% from the prior three months.

December 7

- Nonfarm payrolls increased 155,000 in November, below economist forecasts of 200,000.

- The unemployment rate was unchanged at 3.7%, as expected, matching the lowest rate since December 1969.

- Selling accelerated as concerns over trade relations between the U.S. and China, particularly in light of yesterday’s Huawei incident, remained at the fore.

December 10

- Indices plunged in the morning session, but managed to recover considerable ground as the session progressed.

- The rebound was led by a rally in tech stocks, as renewed confidence in the economy’s strength offset worries about U.S.-China trade disputes.

- Investors remained on edge about global economic growth, as British PM Theresa May announced a decision to postpone an important Brexit vote.

December 11

- Stocks opened higher this morning, slipped into negative territory by the end of the session.

- Leadership was found in the technology and consumer names, in contrast to weakness in the industrials and financial issues.

- The Producer Price Index moved up 0.1% in the month of November, while the core figure rose 0.3% for the period. These readings suggested that inflation was not yet becoming a major problem.

December 12

- Markets closed lower after volatile trading session which saw indices oscillating between positive and negative territory.

- Stocks initially advanced due to President Trump’s positive comments regarding trade negotiations with China.

- As investors assessed US-China tensions, the markets reflected the overall conclusive sentiment in the last half hour of trading, wherein indices fell sharply.

December 13

- Initial jobless claims decreased 27,000 to a seasonally adjusted 206,000 in the week ended December 8, beating economists expectations of 225,000 new claims.

- Indices started trading higher on news that China’s government had bought around 500,000 tons of soybeans from the US.

- Yet sentiment began trailing off toward the end of the session, causing the markets to give up much of the day’s gains.

December 14

- Weak economic data from China and Europe pressured stock index futures globally.

- China’s monthly retail sales grew at its weakest rate in 15 years and industrial output rose the least in almost three years while a purchasing managers index in the euro zone fell.

- There was news that China will suspend additional tariffs on U.S. made vehicles and auto parts for three months starting January 1, 2019.

- U.S. retail sales increased a seasonally adjusted 0.2% in November, which compares to expectations of a 0.1% gain.

- November industrial production increased 0.6%, which compares to the anticipated gain of 0.3% and November capacity utilization was 78.5% when 78.6% was estimated.

December 17

- Indices hit new record lows as investors gave greater weight to indications of slower economic growth and the effects of unresolved trade tensions with China.

- The US said China’s unfair competitive practices were harming foreign companies and workers in a way that violates WTO rules.

- Adding to widespread investor pessimism, the Empire State manufacturing survey significantly fell in December, declining to 10.9, which is down from 23.3 in November; economists were expecting 20.1.

December 18

- All three indices collapsed again as investors remained wary of the Fed’s widely expected fourth rate hike for 2018 in addition to the absence of any positive news on the trade front.

- Housing starts increased 3.2% in November from the prior month to a seasonally adjusted annual rate of 1.256 million.

- In a CNN Business interview, Greenspan mentions that market may still have some time to run upwards but then warns “at the end of that run, run for cover.”

December 19

- Indices took a dive after Federal Reserve officials delivered their fourth rate hike of 2018 and Fed Chairman Jerome Powell signaled that the central bank would continue to unwind its balance sheet at the current rate.

- The consumer discretionary sector led S&P 500 declines

- Powell also emphasized uncertainty around the forecasts from today’s statement, namely weaker global growth and tighter financial conditions, while asserting that these developments have not fundamentally altered the Fed’s outlook.

December 20

- All US indices fell sharply after witnessing a highly volatile session following the Fed’s decision to hike rates for the fourth time this year.

- Investors opted for panic selling despite the fact that the central bank hinted at a more dovish stance in 2019 as well as positive developments on the U.S.-China trade war front.

- Existing-home sales came in at a seasonally adjusted annual rate of 5.32 million, beating the consensus estimate of 5.2 million.

- The U.S. trade deficit increased to $124.8 billion in the third quarter of 2018 compared with $101.2 billion the second quarter.