Upcoming Government Reports & Holidays

| Mar 01 | CONSTRUCTION SPENDING REPORT |

| Mar 04 | MANUFACTURERS’ SHIPMENTS, INV… – FULL REPORT |

| Mar 05 | EMPLOYMENT SITUATION REPORT |

| Mar 05 | US INTERNATIONAL TRADE IN GOODS & SERVICES… |

| Mar 08 | MONTHLY WHOLESALE TRADE: SALES & INV… |

| Mar 10 | CONSUMER PRICE INDEX REPORT |

| Mar 10 | BUSINESS FORMATION STATISTICS |

| Mar 12 | PRODUCER PRICE INDEX REPORT |

| Mar 12 | QUARTERLY SERVICES SURVEY |

| Mar 16 | ADVANCE MONTHLY SALES FOR RETAIL & FOOD… |

| Mar 16 | MANUFACTURING AND TRADE: INVENTORIES & SA… |

| Mar 17 | NEW RESIDENTIAL CONSTRUCTION REPORT |

| Mar 22 | QUARTERLY FINANCIAL REPORT: MANUFACTURING… |

| Mar 22 | QUARTERLY FINANCIAL REPORT: RETAIL TRADE |

| Mar 23 | NEW RESIDENTIAL SALES REPORT |

| Mar 24 | ADVANCE REPORT ON DURABLE GOODS – MAN… |

| Mar 25 | PRELIMINARY US IMPORTS FOR CONS… STEEL… |

| Mar 26 | ADVANCE ECONOMIC INDICATORS REPORT |

Key Events That Moved the Market in Feb 2021

The following is a review of US and world events from the last month. Please be advised that this content is based upon the opinions and research of GFF Brokers and its staff and should not be treated as trade recommendations.

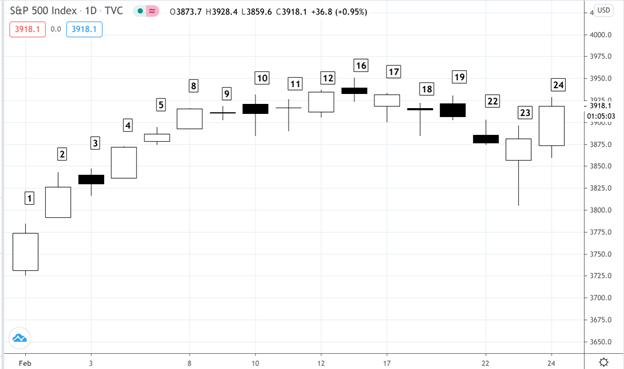

S&P 500 – Daily Chart – Feb 1-24, 2020 (Source: Tradingview)

Monday – February 1

- The short-squeeze fever broke, allowing the broader market to gain some footing a recoup slightly after last week’s pullback.

- The PMI Manufacturing index came in at 59.2, slightly higher than the expected consensus figure of 58.0.

- The ISM manufacturing index, in contrast, slipped lower, coming in at 58.7 missing 60.0 estimates.

- Construction spending rose to 1.0%, beating 0.8% estimates but well within the expected range.

Tuesday – February 2

- Stocks move higher as heavily shorted stocks gave way to dip-buying mostly in blue-chip growth companies.

- There were no major economic reports today.

Wednesday – February 3

- Pulling back from the precious two day’s rallies, investors held back today.

- The ADP employment report showed a strong rebound of 174,000, easily beating consensus estimates of 50,000.

Thursday – February 4

- With a fourth straight day of gains, the market completed a nine-day round trip back into record-high territory.

- Jobless claims saw some relief in continued declines, coming in at 779,000 new claims, far below expectations of 835,000.

- Non-farm productivity saw a decline of -4.8%, lower than the -2.8% consensus, while costs soared to 6.8%, doubling that of the 3.5% consensus estimates.

Friday – February 5

- The broader stock market is climbing with the major averages trying to finish their best week since November.

- Investors may be hoping that the disappointing January jobs report might increase the likelihood of further stimulus.

- Job growth returned to the U.S. in January, with nonfarm payrolls increasing by 49,000.

- The unemployment rate fell to 6.3%, the Labor Department said Friday in the first employment report of the Biden administration.

Monday – February 8

- The path of least resistance remains higher as the broad market indexes logged gains up a few notches on almost very little economic news.

Tuesday – February 9

- Markets took a pause with investors digesting the gains amid promising economic news, all of which contributed to a good start for the month.

- Jobs in December rose to 6.646 million, higher than the 6.4 million expected, according to the latest JOLTS report.

Wednesday – February 10

- Markets continue to hold steady as January’ CPI came in at a consensus 0.3%.

- Jerome Powell spoke today, mentioning that the Bureau of Labor and Statistics’ unemployment figure of 6.3% was miscalculated; the real rate is closer to 10%.

Thursday – February 11

- Indexes slid lower as the jobless claims once again took a turn for the worse.

- 793,000 jobs were lost last week, higher than the estimated 760,000.

- The Fed balance sheet grew by another $31.6 billion for the week ending February 10.

Friday – February 12

- Markets are hovering their record highs to end the week on a positive note.

- Consumer sentiment came in at 76.2, slightly lower than the anticipated figure of 79.0; boosted (or slowed?) in part by varying progress in vaccinations rollouts amid new strains of Covid affecting the country.

Monday – February 15

- Markets closed – Presidents Day Holiday

Tuesday – February 16

- Stocks took a pause while treasury yields zoom higher as investors price in a livelier economy come Spring.

- The Empire State manufacturing index came with a surprise at 12.1, beating expectations of 5.7.

Wednesday – February 17

- Another choppy day for the markets, the Dow Jones ended up closing at a new high as a strong batch of economic data before the open set a backdrop for today’s market action.

- Strong retail sales showed a big jump in January, likely boosted by a big stimulus from Washington.

- US producer prices also came in higher, its sharpest increase since 2009.

- Although the jump of 1.3% versus 0.4% month over month and 1.7% year over year versus the anticipated 0.9% is good news for the economy, it highlighted concerns about inflation.

- Industrial production numbers came in at 0.9%, lower than the 1.3% consensus while capacity utilization at 75.6% came in slightly higher than 74.9%.

Thursday – February 18

- Another market dip and partial recovery as investors digest recent gains in light of the worse-than-expected jobless claims data.

- 861,000 jobs were lost last week, more than the expected 848,000.

- The Philly Manufacturing Index came in at 23.1, higher than the expected range of 20.0.

- Although housing starts at 1.580 million came in lower than expectations of 1.655 million, housing permits at 1.881 million came in higher than the expected 1.670 million consensus figure.

Friday – February 19

- Markets are all rising as Janet Yellen calls for a bigger fiscal stimulus.

- January home sales of 6.690 million shot above December’s 6.650 million, a 23.4% year over year increase.

- PMI composite shifted upward to 58.8, more or less in line with expectations of 58.7.

Monday – February 22

- Stocks were weaker at the open but ended off session lows.

- The S&P 500 had fallen for a fifth straight day, its longest losing streak since last February.

- Treasury Secretary Janet Yellen has been pounding the table for a large stimulus bill, and the House is moving forward with the proposed $1.9 trillion bill.

- Not all sectors are favorably exposed to the “reflation trade,” specifically tech stocks which have been tumbling for a few weeks.

Tuesday- February 23

- The S&P 500 finally snapped its 5-day losing streaks as the markets rallied to the close of a rocky start.

- Rates were a big perry until Fed Chief Jerome Powell assured in his testimony before Congress that the Fed more or less has the market’s back–meaning, low rates for an extended period of time.

- Consumer confidence came in at 91.3, higher than the anticipated 9.0.

Wednesday – February 24

- The stock market staged a huge intraday comeback as investors continued to piled into names sensitive to an economic recovery, while looking past the risk of inflation and rising interest rates.

- Currently, the Dow jumped up 430 points, the S&P 500 advanced 1.1%, and the tech-heavy Nasdaq Composite erased a 1.3% loss and turned 0.9% higher.

- New home sales are also sharply higher at 923,000 as compared with expectations of 855,000.